Back in September 2018 I suggested that Spotify faced a Tencent risk,with the potential of Tencent launching a competitive offering in markets that Spotify is not yet in. This would effectively divide the world between Spotify in Europe, Americas and some of Asia, and Tencent potentially everywhere else. Since then, Tencent has been distracted by acquiring a 10% stake in Universal Music. The fact it is now reportedly looking for partners to share the investment could point to Tencent getting spooked by slowing streaming growth in the second half of the year, something MIDiA predicted in November last year. Meanwhile, as all this was happening, Bytedance’s TikTok has become a global phenomenon – adding 500 million users in 2019 to reach 1.2 billion in total. On the back of this success, Bytedance has picked up Tencent’s dropped baton and has been working on a subscription service that now looks set for a December launch. The streaming market desperately needs a breath of fresh air; the only question is whether music rights holders feel bold enough to let Bytedance launch something truly market changing.

Change, but remain the same

TikTok has undeniable scale, even though the 1.5 billion figure likely refers to installs rather than active users. While it is certainly bigger than previous music messaging apps, the tech graveyard is full of once-promising, now-dead or near-obsolete ones (Musical.ly, Flipagram, Dubsmash, Ping Tunes, Music Messenger etc). In order to ensure it does not go the way of its predecessors (i.e. burn bright but fast) TikTok must learn how to expand and evolve its content offering but remain true to its users’ core use cases. The smart digital content businesses do this. Facebook and YouTube have both dramatically changed their content mixes since launch, yet fundamentally meet the same underlying use cases they started out with. It is essential for TikTok to ensure it grows with its young audience in the way Instagram has – otherwise it risks following the unwelcome path of its predecessors.

Do first, ask forgiveness later

The three global-scale consumer music apps which are genuinely differentiated from the rest of the streaming pack are YouTube, Soundcloud and TikTok. All three have one thing in common: they did first and asked forgiveness later. Rather than coming to music rightsholders to acquire rights and then building platforms around whatever rights they were able to secure, they built apps, built scale and then entered into serious licensing conversations. Crucially, they did so from a position of strength. The rest managed to secure fundamentally the same sets of rights, resulting in a marketplace of streaming services that lack differentiation. They all have the same catalogue, pricing and device support. They are even competing largely in the same markets. They are forced to differentiate with extras, such as playlists, personalisation and branding. This contrasts sharply with the highly-differentiated streaming video market and is the equivalent of the automotive market telling everyone they have to buy a Lexus but can choose what colour paint they want. Those three disruptors did exactly that: they disrupted, and in doing so fast-forwarded the rate of innovation.

The music market needs Bytedance to do something transformational

This is the context in which Bytedance is building a music subscription service. What the music market really needs is for this to be something that builds on the ethos and use cases of TikTok rather than becoming a cookie-cutter “all you can eat” service. Soundcloud and YouTube both found themselves dumbing down their core propositions in order to launch music subscriptions. Now, with streaming growth slowing, the market needs a disruption more than ever. It needs a Plan B to reinvigorate growth.

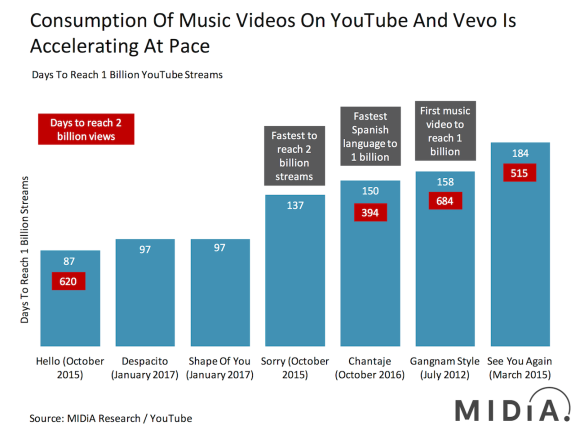

It is all too easy to say that rights holders have held back the market, and in some respects they have. But they also have an obligation to protect their rights and core revenue source: streaming. Indeed, there is an argument that YouTube is currently holding back streaming potential by delivering such a compelling free proposition – something that would not have happened if it had licensed first and launched later.

Emerging markets testbed

Music experiences from China, Japan and South Korea look very different from the ones that have come from the West, whether you are looking at Tencent’s music apps or K-pop artists. While there is a temptation to say that these reflect the unique cultural make ups of their respective markets, in all probability much of it will export. Indeed, we already see this happening with the success of BTS and of course TikTok in Western markets. What unifies these experiences is monetising fandom rather than consumption (which is what Western services do). The problem is that it is difficult for music rightsholders to agree with digital service providers (DSPs) on how much of the assets monetised in fandom platforms should bear royalty income, and just how much. This is one of the main stumbling blocks in monetising fandom.

Emerging markets may be the perfect testbed. We have already seen this approach in Brazil, where Deezer launched a prepay carrier-billing-integrated 60% discounted music bundle with local carrier TIM and has enjoyed strong subscriber growth as a result. The fact that Bytedance may launch first in emerging markets such as India, Indonesia and Brazil suggests that this approach may be being followed. If so, there is a chance that we might see something genuinely innovative coming to market.

While this may not yet constitute the Tencent risk model, there nonetheless remains a chance that Bytedance could end up being an emerging market counterweight to the Western market incumbents. The streaming market needs something new to up the innovation ante; let’s hope Bytedance can take on that mantle…