Today MIDiA Consulting is proud to announce the publication of an important new report: The Death of the Long Tail: The Superstar Music Economy. The report is available free of charge to Music Industry Blog subscribers. (If you are not yet a subscriber to this blog simply enter your email address in the box on the right hand column of the home page.)

Today MIDiA Consulting is proud to announce the publication of an important new report: The Death of the Long Tail: The Superstar Music Economy. The report is available free of charge to Music Industry Blog subscribers. (If you are not yet a subscriber to this blog simply enter your email address in the box on the right hand column of the home page.)

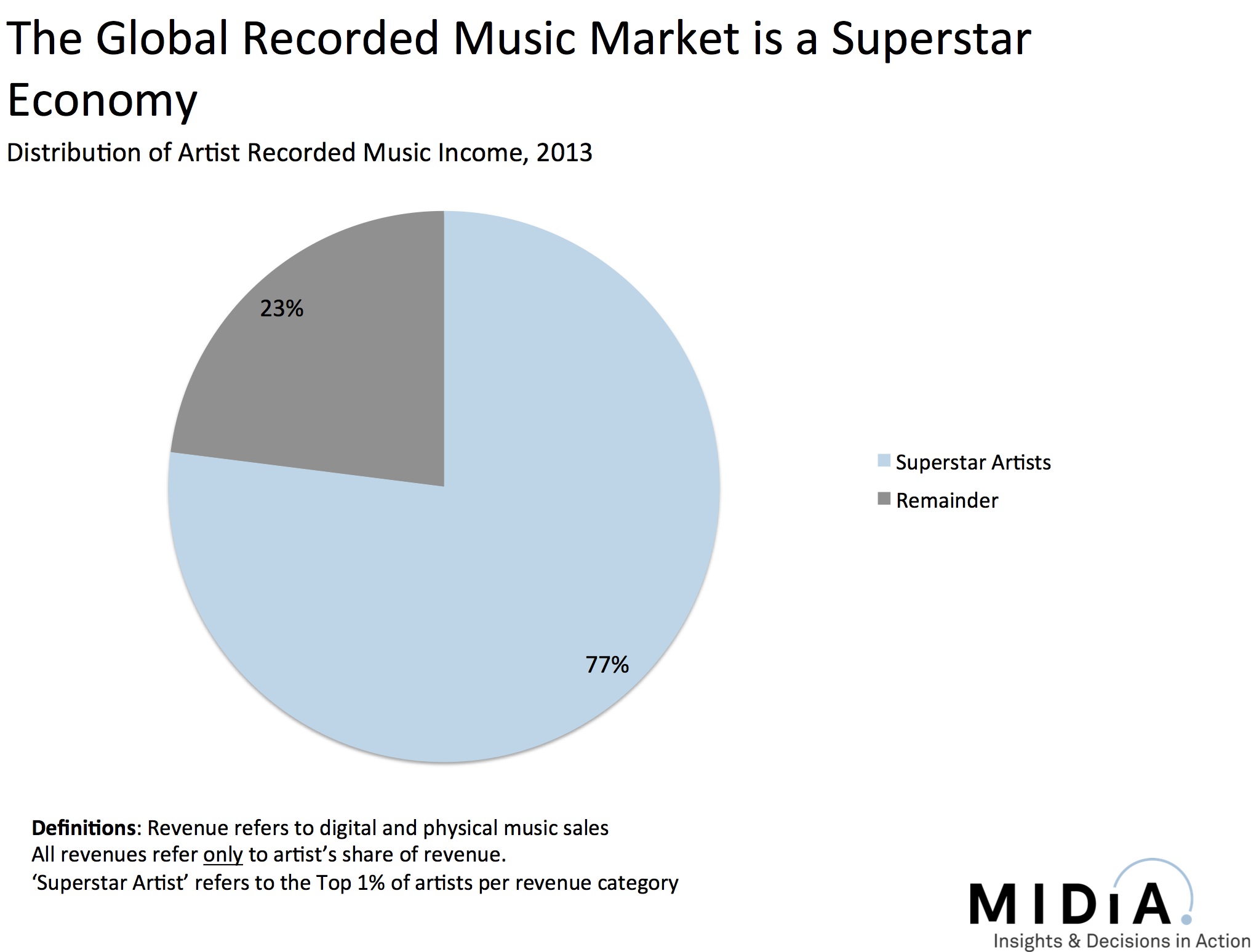

The 21st century decline in recorded music revenues continues to send shockwaves throughout the music industry and although there are encouraging signs of digital-driven growth, the impact on artists is less straightforward. Total global artist income from recorded music in 2013 was $2.8 billion, down from $3.8 billion in 2000 but up slightly on 2012. Meanwhile artists’ share of total income grew from 14% in 2000 to 17% in 2013. But the story is far from uniform across the artist community.

The Superstar Artist Economy

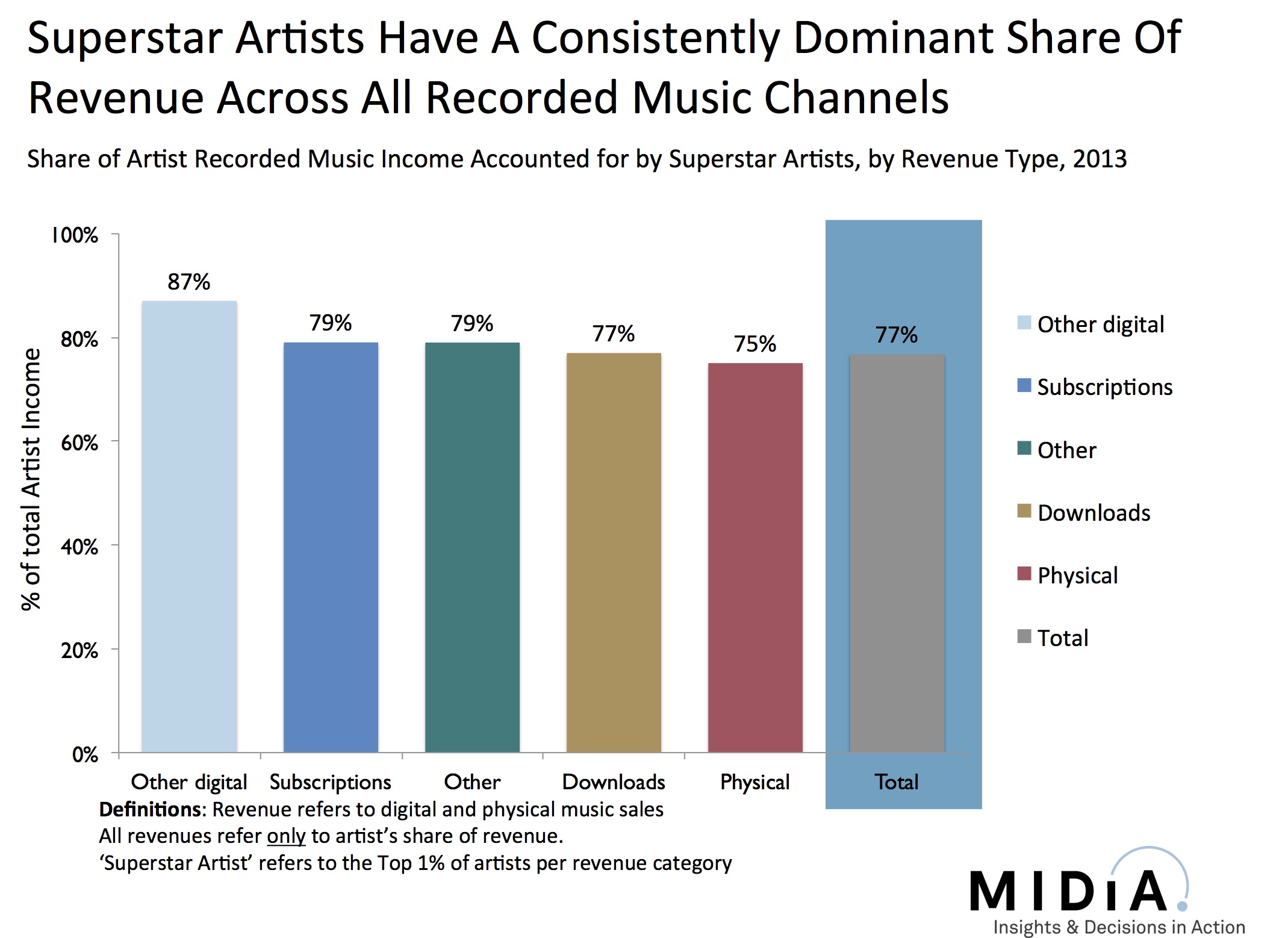

The music industry is a Superstar economy, that is to say a very small share of the total artists and works account for a disproportionately large share of all revenues. This is not a Pareto’s Law type 80/20 distribution but something much more dramatic: the top 1% account for 77% of all artist recorded music income (see figure).

The concept of the long tail seemed like a useful way of understanding how consumers interact with content in digital contexts, and for a while looked like the roadmap for an exciting era of digital content. Intuitively the democratization of access to music – both on the supply and demand sides – coupled with vastness of digital music catalogues should have translated into a dilution of the Superstar economy effect. Instead the marketplace has shown us that humans are just as much wandering sheep in need of herding online as they are offline.

In fact digital music services have actually intensified the Superstar concentration, not lessened it (see figure). The top 1% account for 75% of CD revenues but 79% of subscription revenue. This counter intuitive trend is driven by two key factors: a) smaller amount of ‘front end’ display for digital services – especially on mobile devices – and b) by consumers being overwhelmed by a Tyranny of Choice in which excessive choice actual hinders discovery.

Ultimately it is the relatively niche group of engaged music aficionados that have most interest in discovering as diverse a range of music as possible. Most mainstream consumers want leading by the hand to the very top slither of music catalogue. This is why radio has held its own for so long and why curated and programmed music services are so important for engaging the masses with digital.

Music has always been a Superstar economy and there will always be winners and losers in music sales, with the big winners winning really big. Over time the improved discovery and programming in digital music services should push the needle for the remainder artist tier but a) it will not happen over night and b) it will still have a finite amount of impact.

The Catalogue Size Arms Race

Matters are worsened by the music services’ catalogue arms race which has become entirely detrimental to consumers’ digital music experiences. Action needs taking urgently to make sense of 25 million songs, not just through discovery and editorial, but also by taking the brave decision to keep certain types of content, such as sound-alikes, outside of music services’ main functionality.

Until labels, distributors and artists come to together to fix the issue of digital catalogue pollution – sound alikes and karaoke especially – the Tyranny of Choice will reign supreme, hiding 99% of artists under a pervasive shroud of obscurity and giving the Superstars another free lap of the track.

This explains a lot to me about the last decade of music. I was actually thinking today about how the death of record stores would obviously compound this issue, as local curators disappear day by day.

Pingback: A Journal of Musical ThingsA Must Read: This Research Goes a Long Way to Explaining the Popularity of Justin Bieber » A Journal of Musical Things

Pingback: La muerte del "Long Tail" por Mark Mulligan | Industria Musical

No suprise. Shift to 50 tune play list on all radio stations is forced by labels desperate for “live” income from super stars. Subscription streaming and advertising around FREE will give us at the best 35 billion industry in 2025. If we switch to discovery moment monetization we will surpass 100B mark before 2020. We need to wake up labels!

Pingback: Digitalisierung führt zu Superstar-Musikwirtschaft statt Demokratisierung | Berlin Mitte Institut - House & Techno Party Blog, Soziologie elektronischer Tanzmusik, Electronic Dance Music

Any word on how to download the actual report? I just subscribed to the email newsletter.

Reblogged this on CREATIVE COMPANION the Blog and commented:

Interesting thoughts about the ‘The Superstar Artist Economy’, what if this was your industry? What could you learn for your industry from these findings?

George could you pls email me at mark AT midiaconsulting DOT COM. Because you have followed me as wordpress follower rather than an email follower I can’t see your email address. I also couldn’t find it on your blog.

Do you have data that goes down below the share of the top 1%? I’d be curious to know what percentage of the total recorded music income pie that the top 10% controls. Is it more than 95% of the total pie?

What is the historic evolution of the revenue share the top 1%. How much was it before the digitalization?

Dries – the report shows the long term trend. Just sign up to the email updates on the home page to get your copy

Pingback: The Top 1% of Artists Earn 77% of Recorded Music Income, Study Finds… | RSS MONSTER

Reblogged this on The Colorado Sound and commented:

While not specific to Colorado music, there’s some good info to be gleaned from this and other similar reports.

Reblogged this on 隠居しました and commented:

ロングテールの終焉

Hi, This sounds interesting. Once I’ve suscribed, how do I get the full report ?

Could you send it to essaigertrude[(at])gmail[(dot )]com

Cheers

Pingback: Digital Music News: The Top 1% of Artists Earn 77% of Recorded Music Income, Study Finds… | RIDDIM DON MAGAZINE

As with the others, I’m very interested in getting the full report! Looks like you’ve done some good work.

I signed up for the e-mail updates, but I’m not getting a confirming e-mail.

Mark, just joined your malling list. How do I get to download the report?

Thanks!

Pingback: Top 1% of artists earn 77% of recorded music income, new report finds | Consequence of Sound

If anyone has signed up to the blog but has not yet received the report please email me at mark AT midiaconsulting DOT COM and I will send the report directly to you.

Reblogged this on Can I May I.

Pingback: The Death of the Long Tail | Can I May I

Pingback: New Report by MIDiA – The Death of the Long Tail | Can I May I

Pingback: Top 1% of artists earn 77% of all music income | GetToTheFront

Pingback: The Top 1% of Artists Earn 77% of Recorded Music Income, Study Finds… | This Industry Thing Of Ours

Pingback: Death of the Musical Long Tail | Mae Mai

Pingback: Study shows 1% of artists earn 77% of the profits

Pingback: Un triste constat pour l’industrie de la musique | TRAX MAGAZINE

Pingback: Le Net rend plus con que la TV

Without an explanation of who the full 100% of artists are, this article of 1% earning 77% has no real basis to compare to the past. My guess is that there are far more people converting recorded music into dollars nowadays, superstars notwithstanding, than at any time in the past. If the 100% of artists includes anyone who has a CD on CDBaby.com/iTunes, then the artist ‘count’ has skyrocketed compared to the artist count in the past. There is no death of the long tail, merely a continual extension of the long tail and a thickening of the long tail.

Watch the BBC’s “Produced by George Martin” and specifically the comments George made about just a handful of hits by the Beatles earning the lions share of revenue for EMI, not just the Parlophone label. The EMI execs questioned him on why that was – why couldn’t he get every single Beatles tune to be a hit, or any of the other artists he produced. That one comment showed an even larger ‘tyranny of the superstar’ than what is now present.

Scott – this data refers to all global artist income, so it is every single artist that is making their music available for purchase.

The phrase ‘death of the long tail’ refers to the theory that the long tail will prosper, rather than to the actual presence of it.

Mark, what Scott says (I think) is that many more people offer their music for money nowadays (because releasing music on the web just doesn’t bring any financial risks). Since there are many more participators, this 1% also becomes a larger group. This would just mean that there are many more ‘superstars’ then there were before. It makes sense that music that didn’t use to be ‘release worthy’ doesn’t sell much, but this music does contribute to shifting more artist into the top 1% in this model. So the shape of the long tail might have changed, but to draw the conclusion that people tend to listen to mainstream music now more then before would be a bit hasty I would say.

Is this was you are saying Jan? Want to make sure I’m following you:

The denominator of the fraction (total artists with releases) keeps getting bigger, but the numerator stays more or less the same (total number of artists making good coin from their recordings).

That’s kind of how I see it. The number of successful people was small back in the day and it’s still small now. But back in the day, only the top 10% of artists were given an opportunity to release a record and there were few releases. Today, anyone can do it. So if we adjust for the inflation in the number of releases, the top 1% of today may not be that different in absolute size than the top 10% was back in the day.

That being said, I do think that there have been some negative shifts at the bottom of today’s top 10%. Maybe that’s purely a function of there being more releases, making it into the top 10% doesn’t mean as much anymore (i.e., it’s akin to being at the bottom of the top 25% percent back in the day.

Hard to say. But by the late 1990s, the cost of CD replication had gotten to the point where just about anyone could release one. Nevertheless, in that period it was still easier for people at the bottom of the top 10% to make some money from their records, put that together with touring and merch sales, and maybe manage a subsistence level full-time living as a musician.

That possibility seems much harder to come by now. So while maybe 91st percentile was good enough to put you in that position at the beginning of the 21st century. Now, perhaps you need to be over the 94th or 95th percentile to get to that same place.

Oops one mistake above. I should have said the following: “but the numerator stays more or less the same or has at least grown more slowing than the denominator has (i.e., total number of artists making good coin from their recordings).

Pingback: The Death of the Long Tail | ok-cleek

Pingback: La coda lunga è corta | Italian Jam

Yes, that is what I meant. I think comparing the top 10% from earlier days with today’s top 1% is a good illustration.

Musical taste is now dictated by television, including festivals of mediocrity like American Idol.

Pingback: Study: The Top 1% of Artists Earn 77% of Recorded Music Income | That Eric Alper

Pingback: New Study Shows That Top 1% of All Artists Earn 77% of Total Record Music Income | HYPETRAK

money know has to be allocated to concerts and media as opposed to unit sales in the early 90’s the big thing here to recognize is that people have to put into account the market is changing. proper infrastructure is necessary in the future for the music industry to be more sustainable

Pingback: Morning Music Notes – The 1% « PeteHatesMusic

Pingback: Rynkiem fonograficznym rządzą supergwiazdy | muzykaiprawo.pl

Pingback: Musique : La domination des artistes stars renforcée par Internet | Digital Business

Pingback: Les artistes amateurs ont-ils vraiment leur chance sur la toile ? | digitalhappyfactory

Pingback: El 1% del total de músicos retiene el 77% del capital generado por la industria musical | Darba Culture

Pingback: Musique en ligne, un moyen de promotion pour un indépendant | MusicMug

Pingback: Musicians: just go home and die! at The Wil Forbis Blog

Pingback: Logic Pro Expert The Music Industry is a Superstar Economy » Logic Pro Expert

Pingback: The death of the long tail? - iMusician Digital

Pingback: Why 1% of Musicians Get 77% of Recorded Music Revenue - No Label No Problem | No Label, No Problem

Pingback: Prince: black people don't get second chances « Music Industry 101

Pingback: New Study Shows Startling Facts About the Music Industry | Smack Water Blog

Pingback: Detritus 297 | Music of Sound

But has this figure (23%) improved over the years considering the pie / total revenues to the ‘remainder’ rising, while the absolute numbers of such indie artists also exploding simultaneously?

It will be great to see the trend line for the past few years on this one. Thanks

These stats on the long tail in the music industry are especially interesting and informative. How do you feel about the recent ‘free-to-stream’ kind of setups like Spotify and Pandora? Do they have different impacts on the long tail in digital distribution of music?

Algunas ρublicaciones me gustaron bastante mas ρero no esta mal Animo!

Pingback: Report Claims 1% Of Artists Account For 77% Of All Record Revenue - Music News, Reviews, Interviews and Culture - Music Feeds

Pingback: Music Industry Economics | New Economy and Media

Pingback: Music Industry Economics | Politics & Economics of Global Media

Pingback: Die Superstar-Economy der Musikindustrie: 75-79% aller Einnahmen gehen an 1% der Artists | Berlin Mitte Institut - House & Techno Party Blog, Soziologie elektronischer Tanzmusik, Electronic Dance Music

Pingback: Música Digital: Oportunidades para artistas y consumidores |

Pingback: Música Digital Oportunidades Para Usuarios y ArtistasFormacion Gerencial

Hi Mark, I’m very interested on the full report. How can I have it? I already joined the mail list but i haven’t received the report yet.

Pingback: Tidal to serwis jednego procenta. Nie z Wall Street, ale z branży muzycznej

Pingback: Whatever happened to the Long Tail? | TechnoLlama

Pingback: The Millennial Dialogue | Millennials and Diversity: the cases of politics, music and religion

Pingback: Only the Head Remains? « Creative Industries: Reinvention Amidst Disruption

Pingback: Sky & Scene – et tilbakeblikk | ballade.no

Pingback: ¿Garantiza el uso de plataformas masivas el éxito en la difusión de contenido? | vivirENbolivia.net

Pingback: Taking Stock of Industries Related to Book Publishing and How That Relates to the Future | Musings and Marvels

Pingback: Taking Stock of Industries Related to Book Publishing and How That Relates to the Future

Pingback: Hooray for the Record Stores! | dirtfarmer.net

Pingback: The Long Tail vs. Streaming – S T A Y I N G / W O K E /

Awesome post! I actually linked your article onto mine that talks about the same concept of long tail but in terms of streaming! And it is so aggravating how the music industry still has a hierarchal structure, you think that because music is so free for expression and creativity that it would be a medium that allowed everyone to cash in but unfortunately, unless you are a Beyoncé or Ed Sheeran of the world there is very small hope for niche musicians to become have a piece of the 1% pie.

Can’t believe I just found you now! Looking forward to reading more of your posts about the music industry.

Pingback: What Music Has In Common With Bookstores And Swiss Watches - MusoPlug

The long tail theory has a problem or flaw or something missing.

“If you order the list of ALL the products by amount sold, the first 20% items of this new list will sell together, less than what the remaining 80% will sell together”

The problem of this is that doenst take into account who is buying what, how are people bying. If ALL the buys from the 80% came from a single specific ULTRA rich person and everyone else just buy something from the top 20% not presenting this info is misleading since it shows important information.

Pingback: When the (Recorded) Music’s Over | Uncivilized Animals

Pingback: Research paper sources – Convergent Media | Divergent Voices

Pingback: Scientifically, Your Favourite Songs are Sh*t (so Don't Sh*t on Buskers) - The Busking Project

Pingback: Bye Spotify, Musisi Mengambil Alih Kepemilikan Dengan Koperasi | KOPKUN Institute

Very interesting research, thank you. I have a question(s) I would like to ask…

I understand this study to essentially say that: Whilst there may be more choices for consumers, owning to a lowering of the barrier to entry for musicians and SME labels, those musicians on the ‘tail’ don’t make enough sales to be viable as businesses, partly because of the demand from Gen X and Y (and Z?) for niche product and partly because of the limited screen space (especially on a phone) that can be given to music discovery and features.

So here is my questions, do you think however, that it could it be said with some degree of confidence that the reality of the net effect is something like In 2019 there are a materially greater number of independent/autonomous (i.e not owned by a major labels etc) viable and professional musicians and labels (making enough money from both recorded music, live gigs and merchandising) then there were in 1999?

Finally, do you (a) think AI, machine learning/ discovery services and user specific home pages can change this and (b) Gen Z will have a latent and imminent demand for more unique ways to define themselves (i.e niche product)?

Sorry, that was actually a few questions!

Many thanks in advance

David

Pingback: Blockbuster – dotcoma

Pingback: Überraschung: Auszahlungen bei YouTube sind fair. - Butterseite