Today MIDiA Consulting is proud to announce the publication of an important new report: The Death of the Long Tail: The Superstar Music Economy. The report is available free of charge to Music Industry Blog subscribers. (If you are not yet a subscriber to this blog simply enter your email address in the box on the right hand column of the home page.)

Today MIDiA Consulting is proud to announce the publication of an important new report: The Death of the Long Tail: The Superstar Music Economy. The report is available free of charge to Music Industry Blog subscribers. (If you are not yet a subscriber to this blog simply enter your email address in the box on the right hand column of the home page.)

The 21st century decline in recorded music revenues continues to send shockwaves throughout the music industry and although there are encouraging signs of digital-driven growth, the impact on artists is less straightforward. Total global artist income from recorded music in 2013 was $2.8 billion, down from $3.8 billion in 2000 but up slightly on 2012. Meanwhile artists’ share of total income grew from 14% in 2000 to 17% in 2013. But the story is far from uniform across the artist community.

The Superstar Artist Economy

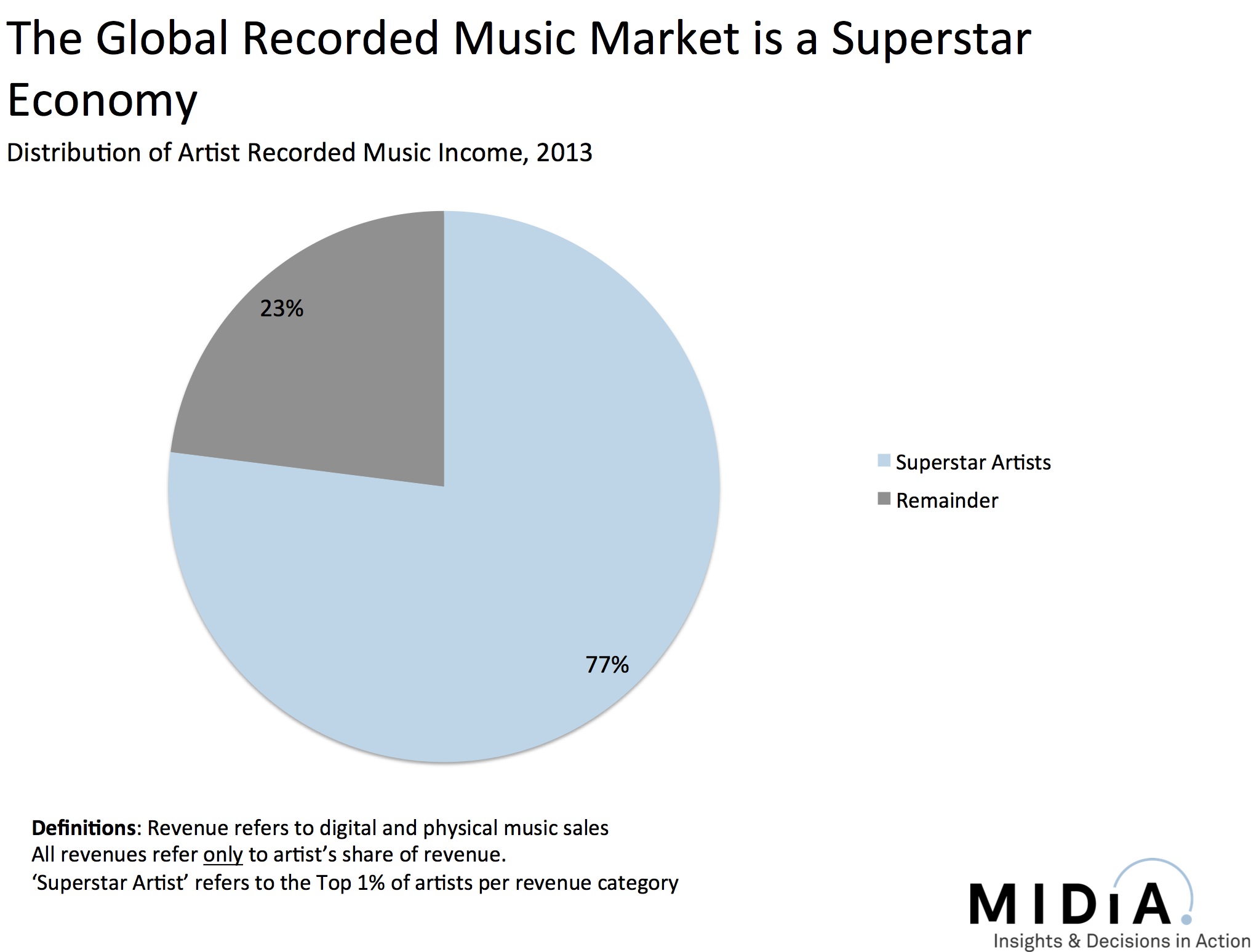

The music industry is a Superstar economy, that is to say a very small share of the total artists and works account for a disproportionately large share of all revenues. This is not a Pareto’s Law type 80/20 distribution but something much more dramatic: the top 1% account for 77% of all artist recorded music income (see figure).

The concept of the long tail seemed like a useful way of understanding how consumers interact with content in digital contexts, and for a while looked like the roadmap for an exciting era of digital content. Intuitively the democratization of access to music – both on the supply and demand sides – coupled with vastness of digital music catalogues should have translated into a dilution of the Superstar economy effect. Instead the marketplace has shown us that humans are just as much wandering sheep in need of herding online as they are offline.

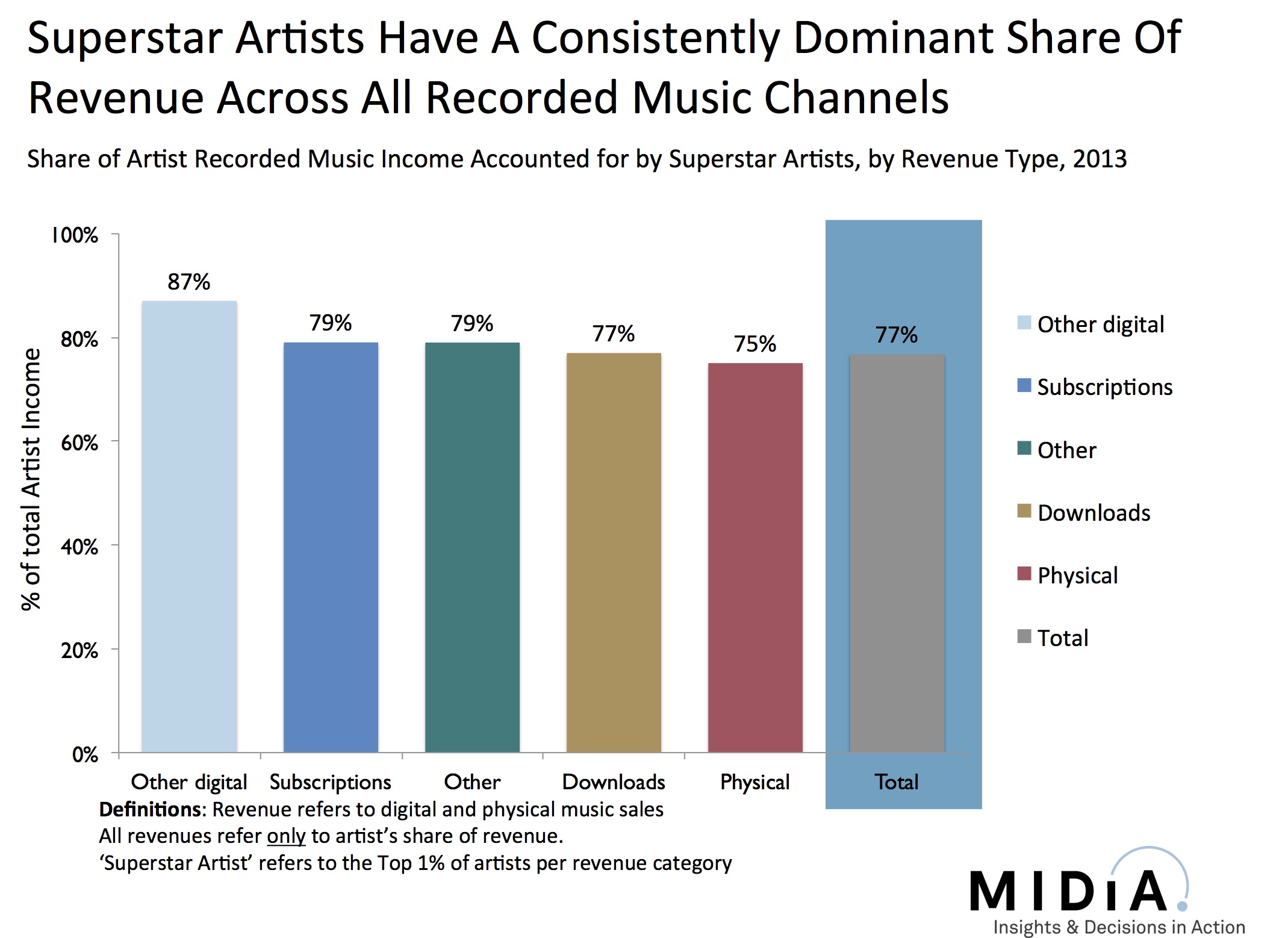

In fact digital music services have actually intensified the Superstar concentration, not lessened it (see figure). The top 1% account for 75% of CD revenues but 79% of subscription revenue. This counter intuitive trend is driven by two key factors: a) smaller amount of ‘front end’ display for digital services – especially on mobile devices – and b) by consumers being overwhelmed by a Tyranny of Choice in which excessive choice actual hinders discovery.

Ultimately it is the relatively niche group of engaged music aficionados that have most interest in discovering as diverse a range of music as possible. Most mainstream consumers want leading by the hand to the very top slither of music catalogue. This is why radio has held its own for so long and why curated and programmed music services are so important for engaging the masses with digital.

Music has always been a Superstar economy and there will always be winners and losers in music sales, with the big winners winning really big. Over time the improved discovery and programming in digital music services should push the needle for the remainder artist tier but a) it will not happen over night and b) it will still have a finite amount of impact.

The Catalogue Size Arms Race

Matters are worsened by the music services’ catalogue arms race which has become entirely detrimental to consumers’ digital music experiences. Action needs taking urgently to make sense of 25 million songs, not just through discovery and editorial, but also by taking the brave decision to keep certain types of content, such as sound-alikes, outside of music services’ main functionality.

Until labels, distributors and artists come to together to fix the issue of digital catalogue pollution – sound alikes and karaoke especially – the Tyranny of Choice will reign supreme, hiding 99% of artists under a pervasive shroud of obscurity and giving the Superstars another free lap of the track.